UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

| Filed by the Registrant ☒ | |

| Filed by a Party other than the Registrant ☐ | |

| Check the appropriate box: | |

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☒ | Definitive Proxy Statement |

| ☐ | Definitive Additional Materials |

| ☐ | Soliciting Material under §240.14a-12 |

AgriFORCE Growing Systems, Ltd.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

| Payment of Filing Fee (Check the appropriate box): | ||

| ☒ | No fee required. | |

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

| (1) | Title of each class of securities to which transaction applies: | |

| (2) | Aggregate number of securities to which transaction applies: | |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

| (4) | Proposed maximum aggregate value of transaction: | |

| (5) | Total fee paid: | |

| ☐ | Fee paid previously with preliminary materials. | |

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |

| (1) | Amount Previously Paid: | |

| (2) | Form, Schedule or Registration Statement No.: | |

| (3) | Filing Party: | |

| (4) | Date Filed: | |

Explanatory note: There are no changes to the 14A except that it is being additionally filed with the tagging Prem14A at the request of the SEC.

AgriFORCE Growing Systems, Ltd.

2233 Columbia Street, Suite 300

Vancouver, BC, Canada V5Y 0M6

November 7, 2022

To the Shareholders of AgriFORCE Growing Systems, Ltd.:

You are cordially invited to attend the Special Meeting of Shareholders (the “Special Meeting”) of AgriFORCE Growing Systems, Ltd., a British Columbia corporation (the “Company”), to be held at 11:00 AM Pacific time on December 8, 2022, at the Company’s principal offices at 2233 Columbia Street, Suite 300, Vancouver, BC, Canada V5Y 0M6.

At the Special Meeting, Shareholders will be asked to consider and vote upon the following proposals:

| 1. | Approve the Company’s July 2022 PIPE Financing. |

| 2. | Approve the September 2022 Stronghold Acquisition. |

| 3. | Approve the October 2022 Manna Acquisition. |

4. |

Approve the acquisition of Delphy Groep BV. |

| 5. | To transact such other business as may be properly brought before the 2022 Special Meeting and any adjournments thereof. |

| 2 |

THE BOARD OF DIRECTORS OF THE COMPANY UNANIMOUSLY RECOMMENDS A VOTE “FOR” APPROVAL OF THE ABOVE FOUR PROPOSALS.

Pursuant to the provisions of the Company’s articles, the board of directors of the Company (the “Board”) has fixed the close of business on November 1, 2022 as the record date for determining the shareholders of the Company entitled to notice of, and to vote at, the Special Meeting or any adjournment thereof. Accordingly, only shareholders of record at the close of business on November 1, 2022 are entitled to notice of, and shall be entitled to vote at, the Special Meeting or any postponement or adjournment thereof.

Shareholders who intend to attend the meeting via teleconference or video conference must submit votes by Proxy ahead of the proxy deadline of 9:00 a.m. (Pacific Time) on December 7, 2022.

The Company reserves the right to take any additional pre-cautionary measures deemed to be appropriate, necessary or advisable in relation to the Meeting in response to further developments related to COVID-19.

Please review in detail the attached notice and proxy statement for a more complete statement of matters to be considered at the Special Meeting.

Your vote is very important to us regardless of the number of shares you own. Whether or not you are able to attend the Special Meeting in person, please read the proxy statement and promptly vote your proxy via the internet, by telephone or, if you received a printed form of proxy in the mail, by completing, dating, signing and returning the enclosed proxy in order to assure representation of your shares at the Special Meeting. Granting a proxy will not limit your right to vote in person if you wish to attend the Special Meeting and vote in person.

| By Order of the Board of Directors: | |

| /s/ Ingo Mueller | |

| Ingo Mueller, | |

| Chairman of the Board of Directors |

| 3 |

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

The 2022 Special Meeting of shareholders (the “Special Meeting”) of AgriFORCE Growing Systems, Ltd. (the “Company”) will be held 11:00 AM Pacific time on December 8, 2022, at the Company’s principal offices at 2233 Columbia Street, Suite 300, Vancouver, BC, Canada V5Y 0M6.

At the Special Meeting, the holders of the Company’s outstanding common shares will act on the following matters:

At the Special Meeting, Shareholders will be asked to consider and vote upon the following proposals:

| 1. | Approve the Company’s July 2022 PIPE Financing. |

| 2. | Approve the September 2022 Stronghold Acquisition. |

| 3. | Approve the October 2022 Manna Acquisition. |

| 4. | Approve the acquisition of Delphy Groep BV. |

| 5. | To transact such other business as may be properly brought before the 2022 Special Meeting and any adjournments thereof. |

Shareholders of record at the close of business on November 1, 2022 are entitled to notice of and to vote at the 2022 Special Meeting and any postponements or adjournments thereof.

Shareholders who intend to attend the meeting via teleconference or video conference must submit votes by Proxy ahead of the proxy deadline of 9:00 a.m. (Pacific Time) on December 7, 2022.

It is hoped you will be able to attend the 2022 Special Meeting but in any event, please vote according to the instructions on the enclosed proxy as promptly as possible. If you are able to be present at the 2022 Special Meeting in person , you may revoke your proxy and vote in person.

| Dated: November 7, 2022 | By Order of the Board of Directors: |

| /s/ Ingo Mueller | |

| Ingo Mueller, | |

| Chairman of the Board of Directors |

| 4 |

AGRIFORCE GROWING SYSTEMS, LTD.

2233 Columbia Street, Suite 300

Vancouver, B.C. V5Y 0M6

SPECIAL MEETING OF SHAREHOLDERS

To Be Held December 8, 2022

PROXY STATEMENT

The Board of Directors of AgriFORCE Growing Systems, Ltd. (the “Company”) is soliciting proxies from its shareholders to be used at the 2022 Special Meeting of shareholders (the “Special Meeting”) to be held at the Company’s offices at the Company’s principal offices at 2233 Columbia Street, Suite 300, Vancouver, BC, Canada V5Y 0M6, and at any postponements or adjournments thereof. This proxy statement contains information related to the Special Meeting. This proxy statement and the accompanying form of proxy are first being sent to shareholders on or about November 10, 2022.

ABOUT THE SPECIAL MEETING

Why am I receiving this proxy statement?

You are receiving this proxy statement because you have been identified as a shareholder of the Company as of the record date which our Board has determined to be November 1, 2022, and thus you are entitled to vote at the Company’s 2022 Special Meeting. This document serves as a proxy statement used to solicit proxies for the 2022 Special Meeting. This document and the Appendixes hereto contain important information about the 2022 Special Meeting and the Company, and you should read it carefully.

Who is entitled to vote at the 2022 Special Meeting?

Only shareholders of record as of the close of business on the record date will be entitled to vote at the 2022 Special Meeting. As of the close of business on the record date, there were 15,713,596 common shares issued and outstanding and entitled to vote. Each holder of common shares is entitled to one vote for each common share held by such shareholder on the record date on each of the proposals presented in this proxy statement.

May I vote in person?

If you are a shareholder of the Company and your shares are registered directly in your name with the Company’s transfer agent, VStock Transfer, you are considered, with respect to those shares, the shareholder of record, and the proxy materials and proxy card, attached hereto as Appendix A, are being sent directly to you by the Company. If you are a shareholder of record, you may attend the 2022 Special Meeting to be held on December 8, 2022, and vote your shares in person, rather than signing and returning your proxy. Only persons attending in person may vote their shares in person.

If your shares of common stock are held by a bank, broker or other nominee, you are considered the beneficial owner of shares held in “street name,” and the proxy materials are being forwarded to you together with a voting instruction card by such bank, broker or other nominee. As the beneficial owner, you are also invited to attend the 2022 Special Meeting. Since a beneficial owner is not the shareholder of record, you may not vote these shares in person at the 2022 Special Meeting unless you obtain a proxy from your broker issued in your name giving you the right to vote the shares at the 2022 Special Meeting.

Photo identification may be required (a valid driver’s license, state identification or passport). If a shareholder’s shares are registered in the name of a broker, trust, bank or other nominee, the shareholder must bring a proxy or a letter from that broker, trust, bank or other nominee or their most recent brokerage account statement that confirms that the shareholder was a beneficial owner of shares of stock of the Company as of the Record Date. Since seating is limited, admission to the meeting will be on a first-come, first-served basis.

Cameras (including cell phones with photographic capabilities), recording devices and other electronic devices will not be permitted at the meeting.

| 5 |

If my Company shares are held in “street name” by my broker, will my broker vote my shares for me?

Generally, if shares are held in street name, the beneficial owner of the shares is entitled to give voting instructions to the broker or nominee holding the shares. If the beneficial owner does not provide voting instructions, the broker or nominee can still vote the shares with respect to matters that are considered to be “routine,” but not with respect to “non-routine” matters, as discussed further below. Your broker will not be able to vote your shares of common stock without specific instructions from you for “non-routine” matters.

If your shares are held by your broker or other agent as your nominee, you will need to obtain a proxy form from the institution that holds your shares and follow the instructions included on that form regarding how to instruct your broker or other agent to vote your shares.

What are “broker non-votes”?

If you hold shares beneficially in street name and do not provide your broker with voting instructions, your shares may constitute “broker non-votes.” “Broker non-votes” occur on a matter when a broker is not permitted to vote on that matter without instructions from the beneficial owner and instructions are not given. These matters are referred to as “non-routine” matters. Since brokers are permitted to vote on “routine” matters without instructions from the beneficial owner, “broker non-votes” do not occur with respect to “routine” matters.

All matters are “non-routine” matters.

The determination of “routine” and “non-routine” matters is determined by brokers and those firms responsible to tabulate votes cast by beneficial owners of shares held in street name and other nominees. Firms casting such votes have generally been guided by rules of the New York Stock Exchange when determining if proposals are considered “routine” or “non-routine”. When a matter to be voted on is the subject of a contested solicitation, banks, brokers and other nominees do not have discretion to vote your shares with respect to any proposal to be voted on.

How do I cast my vote if I am a shareholder of record?

The link for the material will be posted on our website: https://ir.agriforcegs.com/news-events/ir-calendar. If you are a shareholder with shares registered in your name with the Company’s transfer agent, VStock Transfer, on the record date, you may vote in person at the 2022 Special Meeting or by going to www.vstocktransfer.com/proxy. Record holders can also vote: via email (vote@vstocktransfer.com), via mail (with the self addressed envelope the transfer agent will provide) or via fax (646) 536-3179.

Whether or not you plan to attend the 2022 Special Meeting, please vote as soon as possible to ensure your vote is counted. You may still attend the 2022 Special Meeting and vote in person even if you have already voted by proxy. For more detailed instructions on how to vote using one of these methods, please see the form of proxy card attached to this Schedule 14A and the information below.

| ● | To vote in person. You may attend the 2022 Special Meeting and the Company will give you a ballot when you arrive. |

| 6 |

| ● | To vote by proxy by fax or internet. If you have fax or internet access, you may submit your proxy by following the instructions provided in this proxy statement, or by following the instructions provided with your proxy materials and on the enclosed proxy card or voting instruction card. | |

| ● | To vote by proxy by mail. You may submit your proxy by mail by completing and signing the enclosed proxy card and mailing it in the enclosed envelope. Your shares will be voted as you have instructed. |

How do I cast my vote if I am a beneficial owner of shares registered in the name of any broker or bank?

If you are a beneficial owner of shares registered in the name of your broker, bank, dealer or other similar organization, you should have received a proxy card and voting instructions with these proxy materials from that organization rather than from the Company. Simply complete and mail the proxy card to ensure that your vote is counted. Alternatively, you may vote by telephone or over the internet as instructed by your broker or other agent. To vote in person at the 2022 Special Meeting, you must obtain a valid proxy from your broker or other agent. Follow the instructions from your broker or other agent included with these proxy materials or contact your broker or bank to request a proxy form.

What constitutes a quorum for purposes of the 2022 Special Meeting?

The Company’s Articles stipulate that holders entitle to vote in person or represented by proxy may do so at the Special Meeting permitting the conduct of business at the meeting. On the record date, there were 15,713,596 shares of Common Stock and 0 shares of preferred stock issued and outstanding and entitled to vote. The Articles state the quorum for transaction of business at the meeting will be at least one shareholder who is present, or who represents by proxy one or more shareholders who, in the aggregate, hold at least 50% of the issued shares entitled to be voted at the meeting. The Articles further provide that if a quorum is not present, the meeting shall be adjourned to the same day in the next week at the same time and place and those persons present and being, or representing by proxy, entitled to attend and vote at the meeting shall be deemed to constitute a quorum, and in all circumstances, the Company will adehere to all minimum quorum requirements under Nasdaq List Rules. Proxies received but marked as abstentions or broker non-votes, if any, will be included in the calculation of the number of votes considered to be present at the meeting for purposes of a quorum. Your shares will be counted toward the quorum at the 2022 Special Meeting only if you vote in person at the meeting, you submit a valid proxy or your broker, bank, dealer or similar organization submits a valid proxy.

Can I change my vote?

Yes. Any shareholder of record voting by proxy has the right to revoke their proxy at any time before the polls close at the 2022 Special Meeting by sending a written notice stating that they would like to revoke his, her or its proxy to the Corporate Secretary of the Company; by providing a duly executed proxy card bearing a later date than the proxy being revoked; or by attending the 2022 Special Meeting and voting in person. Attendance alone at the 2022 Special Meeting will not revoke a proxy. If a shareholder of the Company has instructed a broker to vote its shares of common stock that are held in “street name,” the shareholder must follow directions received from its broker to change those instructions.

Who is soliciting this proxy – Who is paying for this proxy solicitation?

We are soliciting this proxy on behalf of our Board of Directors. The Company will bear the costs of and will pay all expenses associated with this solicitation, including the printing, mailing and filing of this proxy statement, the proxy card and any additional information furnished to shareholders. In addition to mailing these proxy materials, certain of our officers and other employees may, without compensation other than their regular compensation, solicit proxies through further mailing or personal conversations, or by telephone, facsimile or other electronic means. We will also, upon request, reimburse banks, brokers, nominees, custodians and fiduciaries for their reasonable out-of-pocket expenses for forwarding proxy materials to the beneficial owners of our stock and to obtain proxies.

| 7 |

What vote is required to approve each item?

The vote required to approve each proposal is: “FOR” votes from the holders of a majority of the shares of the Company’s common stock present in person or represented by proxy and entitled to vote on the matter at the 2022 Special Meeting are required to approve each proposal.

Will My Shares Be Voted If I Do Not Return My Proxy Card?

If your shares are registered in your name or if you have stock certificates, they will not be voted if you do not return your proxy card by mail or vote at the Special Meeting. If your broker cannot vote your shares on a particular matter because it has not received instructions from you and does not have discretionary voting authority on that matter, or because your broker chooses not to vote on a matter for which it does have discretionary voting authority, this is referred to as a “broker non-vote.” The New York Stock Exchange (“NYSE”) has rules that govern brokers who have record ownership of listed company stock (including stock such as ours that is listed on The Nasdaq Capital Market) held in brokerage accounts for their clients who beneficially own the shares. Under these rules, brokers who do not receive voting instructions from their clients have the discretion to vote uninstructed shares on certain matters (“routine matters”), but do not have the discretion to vote uninstructed shares as to certain other matters (“non-routine matters”). Neither proposal herein is a routine matter.

If your shares are held in street name and you do not provide voting instructions to the bank, broker or other nominee that holds your shares the bank, broker or other nominee does not have authority to vote your unvoted shares on any of the other proposals submitted to shareholders for a vote at the Special Meeting. We encourage you to provide voting instructions. This ensures your shares will be voted at the Special Meeting in the manner you desire.

Can I access these proxy materials on the Internet?

Yes. The Notice of Special Meeting, and this proxy statement and the Appendix hereto are available for viewing, printing, and downloading at https://ir.agriforcegs.com/news-events/ir-calendar. All materials will remain posted on https://ir.agriforcegs.com/news-events/ir-calendar at least until the conclusion of the meeting.

What should I do if I receive more than one set of voting materials?

You may receive more than one set of voting materials, including multiple copies of this proxy statement and multiple proxy cards or voting instruction cards. For example, if you hold your shares in more than one brokerage account, you may receive a separate voting instruction card for each brokerage account in which you hold shares. If you are a shareholder of record and your shares are registered in more than one name, you will receive more than one proxy card. Please vote your shares applicable to each proxy card and voting instruction card that you receive.

| 8 |

How can I find out the results of the voting at the Special Meeting?

Preliminary voting results will be announced at the Special Meeting. Final voting results will be published in a Current Report on Form 8-K filed with the Securities and Exchange Commission within four business days of the 2022 Special Meeting.

What interest do officers and directors have in matters to be acted upon?

No person who has been a director or executive officer of the Company at any time since the beginning of our fiscal year, and no associate of any of the foregoing persons, has any substantial interest, direct or indirect, in any matter to be acted upon.

Who can provide me with additional information and help answer my questions?

If you would like additional copies, without charge, of this proxy statement or if you have questions about the proposals being considered at the 2022 Special Meeting, including the procedures for voting your shares, you should contact Richard Wong, the Company’s CFO, by telephone at 604-757-0952.

Why is the Company Seeking Shareholder Approval of Matters 1-4?

Nasdaq Listing Rules 5635(a) and (d) require shareholder approval of acquisitions where 20% or more of the shares of Common Stock of the issuer are to be issued as consideration and where 20% or more of the shares of Common Stock of the Issuer are to be issued below the Nasdaq Minimum Price. As Nasdaq Rules aggregate all transactions which occur in a short period of time elapsed, the Company is seeking shareholder approval of the transactions and issuance of shares with regard to all three acquisitions set forth herein as well as the financing described herein.

Householding of Annual Disclosure Documents

The SEC previously adopted a rule concerning the delivery of annual disclosure documents. The rule allows us or brokers holding our shares on your behalf to send a single set of our annual report and proxy statement to any household at which two or more of our shareholders reside, if either we or the brokers believe that the shareholders are members of the same family. This practice, referred to as “householding,” benefits both shareholders and us. It reduces the volume of duplicate information received by you and helps to reduce our expenses. The rule applies to our annual reports, proxy statements and information statements. Once shareholders receive notice from their brokers or from us that communications to their addresses will be “householded,” the practice will continue until shareholders are otherwise notified or until they revoke their consent to the practice. Each shareholder will continue to receive a separate proxy card or voting instruction card.

Those shareholders who either (i) do not wish to participate in “householding” and would like to receive their own sets of our annual disclosure documents in future years or (ii) who share an address with another one of our shareholders and who would like to receive only a single set of our annual disclosure documents should follow the instructions described below:

| ● | shareholders whose shares are registered in their own name should contact our transfer agent, VStock Transfer LLC, and inform them of their request by calling them at (212) 828-8436 or writing them at 18 Lafayette Pl, Woodmere, NY 11598. |

| ● | shareholders whose shares are held by a broker or other nominee should contact such broker or other nominee directly and inform them of their request, shareholders should be sure to include their name, the name of their brokerage firm and their account number. |

| 9 |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

The following table sets forth information known to us regarding the beneficial ownership of our common stock as of November 1, 2022 by:

| ● | each person known to us to be the beneficial owner of more than 5% of our outstanding common stock; |

| ● | each of our executive officers and directors; and |

| ● | all of our executive officers and directors as a group. |

| Common shares | Options vested within 60 days of October 19, 2022 | Warrants | Series A Preferred Shares | Total | Percentage beneficially owned | |||||||||||||||||||

| Directors and Officers: | ||||||||||||||||||||||||

| Ingo Mueller | 1,023,577 | a | 152,771 | - | - | 1,176,348 | 7.4 | % | ||||||||||||||||

| Richard Wong | 120,899 | 61,754 | - | - | 182,653 | 1.2 | % | |||||||||||||||||

| Troy McClellan | 437,120 | 48,659 | - | - | 485,779 | 3.1 | % | |||||||||||||||||

| Mauro Pennella | 32,773 | 18,480 | - | - | 51,253 | 0.3 | % | |||||||||||||||||

| John Meekison | 43,208 | 23,801 | - | - | 67,009 | 0.4 | % | |||||||||||||||||

| David Welch | 52,450 | 19,291 | - | - | 71,741 | 0.5 | % | |||||||||||||||||

| Amy Griffith | - | 8,216 | - | - | 8,216 | 0.1 | % | |||||||||||||||||

| Richard Levychin | - | 8,216 | - | - | 8,216 | 0.1 | % | |||||||||||||||||

| Total all officers and directors (8 persons) | 1,710,027 | 341,188 | 2,051,215 | 13.1 | % | |||||||||||||||||||

| 5% or Greater Beneficial Owners | ||||||||||||||||||||||||

| Ingo Mueller | 1,023,577 | a | 152,771 | - | - | 1,176,348 | 7.4 | % | ||||||||||||||||

| Arni Johannson | 823,615 | b | - | 823,615 | 5.2 | % | ||||||||||||||||||

| Canadian Nexus Team Ventures Corp | 583,278 | - | 317,243 | - | 900,521 | 5.6 | % | |||||||||||||||||

| (a) | Includes (1) 92,030 common shares held by St. George Capital Corp. of which Mr. Mueller is the President, (2) 421,053 common shares held by 1071269 BC Ltd. of which Mr. Mueller is the sole owner, and (3) 31,579 common shares held by 1178196 BC Ltd. of which Mr. Mueller is an affiliate. | |

| (b) | Includes 48,710 common shares held by Canadian Nexus Ventures Ltd. of which Mr. Johannson is the President. |

| 10 |

PROPOSAL NO. 1

APPROVAL OF THE DEBT FINANCING AND ISSUANCE OF SHARES PURSUANT TO THE COMPANY’S JULY 2022 DEBT FINANCING

July 2022 Debt Financing

On June 30, 2022, AgriForce Growing Systems, Ltd. (the “Company”) entered into a Securities Purchase Agreement (“SPA”) with two institutional investors (“Investors”) with an initial purchase of $14.025 million principal amount of debentures (“Debentures”) and accompanying warrants (“Warrants”) and up to an additional $33 million principal amount of Debentures and accompanying Warrants. Under the SPA, the Company received an initial amount of $12.75 million (gross of fees which will be deducted from that amount) on July 6, 2022 and has the right to receive up to an additional aggregate of $33.0 million at the discretion of each of the purchasers hereunder (the “Investors”), in one or multiple tranches, subject to certain conditions, at then-current market prices in minimum tranches of $5 million each. The SPA contains industry standard representations and warranties and negative covenants, including, but not limited to, limitations upon the amounts of indebtedness and other securities which may be incurred and issued by the Company under certain circumstances as set forth in the SPA.

The initial conversion price of the Debentures is $2.22 per share. The Debentures are due in 2.5 years from June 30, 2022, which may be extended for an additional six month period by the Company by paying, at the end of the 18th month of the term of the Debentures, six months of interest at the rate of 8% per annum. The Debentures are subject to a 10% original issue discount and bear interest at 5% for the first 12 months, 6% for the next 12 months and 8% until maturity. The Debentures amortize over a 25 month period commencing on September 1, 2022, and the monthly amortization of the Debentures are payable in cash only for the first 12 months of amortizations and in cash or stock thereafter at the option of the Company. Once the monthly amortizations are payable in cash or stock, the Company can only elect to pay the monthly amortization in stock if certain equity conditions, as set forth in the Debentures, are met, which include, but are not limited to, for each Trading Day in a period of 20 consecutive Trading Days prior to the applicable date in question, the daily trading volume for the Common Stock on the principal Trading Market exceeds $1,000,000 per Trading Day, the Company is not in default of any of its obligations under the Debentures, there is an effective registration statement for the resale of shares issuable under the Debentures, and the Company is in compliance with all Nasdaq listing requirements. The Debentures contain commercially standard events of default and covenants and the like.

In addition, the Investors have received 3.5-year Warrants with 65% warrant coverage at an initial exercise price of $2.442 per share, subject to customary adjustments, including a price ratchet (to the price of the new issuance) if it issues its common shares at a price less than the then in effect exercise price and are subject to standard pro rata dilution for reverse stock splits and the like. The Debentures have the same dilution protection as the Warrants.

Both the Debentures and Warrants contain exercise limitations upon an Investor beneficially owning more than either 4.99% or 9.99% of the Company’s common shares and also contain caps upon the total amount of common shares issuable upon conversion of the Debentures and exercise of the Warrants of 19.9% of the issued and outstanding shares of the Company at the time of the closing of the transactions, until shareholder approval of both the financing transaction, including all subsequent tranches of the financing, and the Delphy acquisition are received, consistent with Nasdaq rules.

| 11 |

The Company has entered into a Registration Rights Agreement with the Investors to register the shares issuable upon conversion of the Debentures and exercise of the Warrants with a registration statement to be filed on Form S-1 no later than 30 days from June 30, 2022 (or any subsequent closing) and effective no later than 60 days from June 30, 2022 (or the date of any subsequent closing; or 90 days, if there is full SEC review). Penalties for missing those deadlines are equal to 2% of the subscription amount per month up to 10% of the subscription amount.

The Company’s subsidiaries have also entered into subsidiary guarantees pursuant to which each guarantees the performance of the Company of its obligations under the SPA and related instruments. Each of the officers and directors has also entered into a lockup agreement to not sell any common shares of the Company owned by each such person for one year from June 30, 2022 (subject to the ability to sell shares received by each as the result of an employment agreement at any time, which ability to sell shares commences on January 1, 2023).

All of the Debentures and Warrants sold under the SPA are sold in private placement transactions exempt from registration under Section 4(a)(2) of the Securities Act of 1933, as amended.

Vote Required

“FOR” votes from the holders of a majority of the shares of the Company’s common stock present in person or represented by proxy and entitled to vote on the matter at the 2022 Special Meeting are required to approve each proposal.

THE BOARD OF DIRECTORS RECOMMENDS A VOTE “FOR”

APPROVAL OF THE DEBT FINANCING AND ISSUANCE OF SHARES PURSUANT TO THE COMPANY’S JULY 2022 DEBT FINANCING

| 12 |

PROPOSAL NO. 2

APPROVAL OF THE STRONGHOLD ACQUISITION AND ISSUANCE OF COMMON SHARES TO BE ISSUED IN THE STRONGHOLD ACQUISITION

As of September 16, 2022, AgriForce Growing Systems, Ltd. (the “Company”) entered into a Purchase and Sale Agreement (“PSA”) with Stronghold Power Systems, Inc. (“Seller”) to purchase approximately 34 acres of land in Coachella California. The purchase price is $4,300,000, payable as follows: (i) $1,500,000 in cash and (ii) $2,800,000 in restricted shares of common stock of the Company. The purchase price is allocable $1,642,350 for purchase of the land and the balance for completion of development work by the Seller on the Property. The stock is being issued in the form of prefunded warrants (pending shareholder approval of issuance of the shares) in two tranches: (i) $1,700,000 (695,866 shares) issued within five days of entry into the PSA, and (ii) $1,100,000 (450,266 shares) at closing of the transaction. The first tranche shall be void if closing of the transaction does not occur by March 31, 2023, and the pre funded per share exercise price is $2.443, and is subject to certain adjustments as stated in the prefunded warrants. Issuance of all securities in this transaction is in transactions exempt from registration under Section 4(a)(2) of the Securities Act of 1933, as amended, and the prefunded warrants bear legends to that effect.

THE BOARD RECOMMENDS A VOTE “FOR”

APPROVAL OF THE STRONGHOLD ACQUISITION AND ISSUANCE OF COMMON SHARES TO BE ISSUED IN THE STRONGHOLD ACQUISITION.

| 13 |

PROPOSAL NO. 3 – APPROVAL OF THE MANNA ACQUISITION AND ISSUANCE OF COMMON SHARES TO BE ISSUED IN THE MANNA ACQUISITION

On September 10, 2021, AgriForce Growing Systems, Ltd. entered into an agreement (“Agreement”) to acquire the intellectual property (IP) from Manna Nutritional Group LLC (MNG), a privately held firm based in Boise, Idaho. The IP encompasses patent-pending technologies to naturally process and convert grain, pulses and root vegetables, resulting in low-starch, low-sugar, high-protein, fiber-rich baking flour products, as well as a wide range of breakfast cereals, juices, natural sweeteners and baking enhancers.

The terms of the Agreement are as follows:

The aggregate purchase price for the Purchased Assets (the “Purchase Price”) is up to $14,475,000, and shall consist of the following, subject to the terms and conditions of this Agreement, as follows:

| (i) | The number of shares of Company’s common stock (rounded up to the nearest whole number), restricted as to resale under Section 4(a)(2) of the Securities Act, equal to the quotient of (i) $5,000,000 divided by (ii) a per share price equal to the average of the volume weighted average price (“VWAP”) of the Company’s common shares for the ten trading days immediately preceding the Due Diligence Deadline (as defined below) (the “Closing Shares”). The Closing Shares, to be due on the Closing Date, which Closing Shares are restricted as to resale and issued under a private placement exempt from registration under Section 4(a)(2) of the Securities Act, are subject to release of restriction and lockup on a quarterly basis over ten quarters commencing on the Closing Date in equal amounts of shares over ten consecutive calendar quarters. The Closing Shares are due and will be issued to MNG upon the date that is 180 days from the Effective Date (September 10, 2021) (the “Due Diligence Deadline”), with such due diligence being comprised of (the following three bullet points are the “KPIs”): |

| ● | Receipt and Tasting of Flours and Sweeteners by the Company; | |

| ● | Independent Lab Testing of Flours and Sweeteners by the Company to confirm fiber, protein, and starch content of such products meets the specifications provided by MNG; and | |

| ● | Completion by the Company of Third-Party Engineering Process Analysis, included in the scope of work outlined by Covert Engineers, dated August 11, 2021, for conceptual and preliminary plant design for a Pilot Manufacturing Facility. |

| (ii) | $1,475,000 in cash, minus any amounts paid to MNG under (iii), payable to MNG at Closing; | |

| (iii) | $725,000 in cash payable follows: (a) $225,000 payable on the Effective Date; and (b) $500,000 payable within 120 days after the Effective Date, to reimburse MNG for, without limitation, satisfaction of all the secured debt as listed in Section 2.04 of the Disclosure Schedules to the Agreement (the “Secured Debt”). |

| 14 |

| (iv) | The number of shares of Company’s common stock (rounded up to the nearest whole number) to be issued in two tranches that equals (i) $8,000,000 divided by (ii) a per share price equal to the VWAP of the Company’s common shares for the ten trading days immediately before the issuance date of those shares (“Post-Closing Shares”). $5,000,000 of the Post-Closing Shares will be issued on June 30, 2022, to be held in Escrow. $3,000,000 of the Post-Closing Shares will be issued to MNG on December 31, 2022, to be held in Escrow. All distributions and dividends attributable to the Post-Closing Shares (collectively, “Dividends”) will accrue for the benefit of MNG and will be held in Escrow pending release of the Post-Closing Shares, in which case all Dividends will be released to MNG at the same time as the Post-Closing Shares are so released. Until Post-Closing Shares are released from Escrow, all voting rights thereto shall be exercised as directed by the Company’s Board of Directors. If a Patent is issued within 24 months of the Closing Date, and such Patent is transferred to the Company free and clear of all encumbrances, then the Post-Closing Shares shall be released from Escrow in four equal amounts commencing on the date of issuance of the Patent and then for the three subsequent three-month anniversaries thereof. |

In the event that after 24 months from the closing date, a Patent does not issue from the IP, Buyer’s obligation to issue the Post-Closing Shares and Dividends to MNG will be deemed null and void ab initio and will no longer be due and owing to MNG, and the Post-Closing Shares shall be released from escrow and returned to the Company, and the Purchase Price shall be adjusted downward dollar for dollar.

As of May 10, 2022, the Company completed an amendment to its asset purchase agreement with Manna Nutritional Group LLC, dated September 10, 2021. The amendment modifies certain provisions of Section 2 thereof. Section 2.04(i) was amended to provide for the issuance of prefunded warrants instead of shares, with the trigger valuation date for the first $3.5 million of equity to be March 10, 2022 and the trigger valuation date for the next $1.5 million of equity to be the resubmission work date on the patents set forth in the asset purchase agreement. Section 2.04(iv) was amended to also reflect issuance of pre funded warrants instead of common shares in two tranches of $5 million on June 30, 2022 and $3 million on December 31, 2022, such that if a Patent (as defined in the asset purchase agreement) is issued within 24 months of the Closing Date (as defined in the asset purchase agreement), then the aforementioned $8 million in prefunded warrants will vest in four equal amounts on the date of issuance of the patent and then for the three subsequent three month anniversaries thereof. If the aforementioned patent does not issue within 24 months of the Closing Date, then those prefunded warrants shall be returned to the Purchaser, and the transaction purchase price shall be adjusted downward, dollar for dollar. The amendment also contains covenants to obtain shareholder approval of the acquisition transactions before the prefunded warrants can be exercised into Company common shares.

On October 17, 2022, the Company closed the assignment of the actual Manna patent and issued to Manna a total of 4,627,675 prepaid warrants which are exercisable into the same number of common shares of the Company upon approval of this Proposal by the Company’s shareholders.

THE BOARD RECOMMENDS A VOTE “FOR” THE APPROVAL OF

THE MANNA ACQUISITION AND ISSUANCE OF COMMON SHARES TO BE ISSUED IN THE MANNA ACQUISITION

| 15 |

PROPOSAL NO. 4 – APPROVAL OF THE DELPHY ACQUISITION AND SHARES TO BE ISSUED IN THE DELPHY ACQUISITION

Delphy Groep BV Acquisition

On February 10, 2022, the Company signed a definitive agreement to acquire Delphy Groep BV (“Delphy”), a Netherlands-based AgTech consultancy firm, for € 23.5 million (USD $23.5 million) through a combination of cash and stock. The closing of the transaction was expected to occur within 60 days of the signing date but is subject to shareholder approval and completion of audited financials of Delphy. The definitive agreement follows the binding letter of intent (“LOI”) as previously announced in the Company’s press release in October 2021. Delphy, which optimizes production of plant-based foods and flowers, has multinational operations in Europe, Asia, Kazakhstan, and Africa, with approximately 200 employees and consultants. Delphy’s client list includes agriculture companies, governments, universities, and leading AgTech suppliers, who turn to the company to drive agricultural innovation, solutions, and operational expertise.

On September 22, 2022, AgriForce Growing Systems, Ltd. (the “Company”) entered into an amendment to its agreement to purchase all of the issued and outstanding shares of Delphy Groep, B.V. Pursuant to the amendment, the total purchase price is reduced from €$23.5 million to €17.66 million (USD $17.66 million), plus a potential earnout of up to €5.99 million (USD $5.99 million) over 2 years, based on achieving future performance milestones. The Company will pay €168,818 of interest on the purchase price (such interest was assessed from May 9, 2022 to July 29, 2022). If closing does not occur by November 15, 2022, the Company will pay additional interest on the purchase price of four percent per annum until closing.

Information on Delphy

Delphy Groep B.V., Wageningen (the “Company” or “Delphy”) is a Netherland based company and was incorporated as a private company by Articles of Incorporation issued pursuant to the provisions of the Dutch Civil Code on October 11, 2005. The Company’s registered and records office address is at Agro Business Park 5, in Wageningen, the Netherlands and is registered at the chamber of commerce under number 09154407. The activities of Delphy Groep B.V. and its group companies (“the Company”) mainly focus on the entrepreneurs in the primary sector and agribusiness partners, both nationally and internationally. Advisors in tree cultivation, pot and bedding plant cultivation, greenhouse vegetables, floriculture, fruit cultivation, strawberry cultivation, field vegetable cultivation, cut flowers, arable farming, flower bulbs and other vegetable sectors, are the confidential advisors on the farm of the agricultural entrepreneur. The two subsidiaries GreenQ Group B.V. and Improvement Centre B.V. operate a modern greenhouse complex, in which new cultivation concepts and technical installations from all parts of the world are developed, tested and demonstrated.

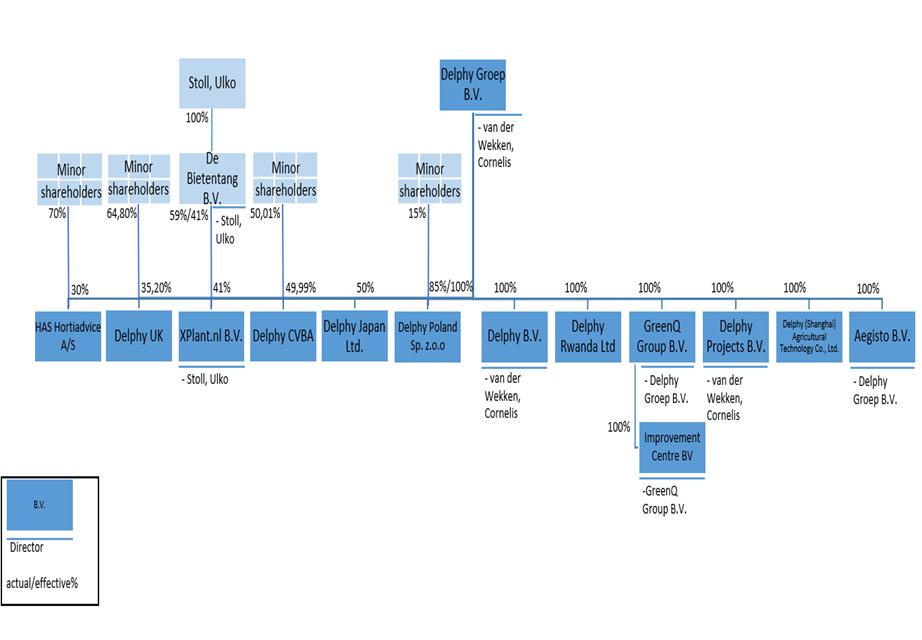

Internal structure

| 16 |

Organizational structure

The Group consists of Delphy Groep B.V. and its Dutch subsidiaries; GreenQ Group B.V. (which in turn serves as an intermediary to Improvement Centre B.V.), Delphy B.V., Delphy Projects B.V. and Aegisto B.V., and its (foreign and Dutch) interests in; Delphy (Shanghai) Agricultural Co. Ltd., Latia Agribusiness Solutions Ltd., Delphy CVBA, Delphy UK Ltd., HAS Hortiadvice A/S, Xplant.nl B.V., Delphy Poland Sp. z.o.o., Delphy Japan Ltd., and Delphy Rwanda Ltd. (a note on the subsidiaries has been added to this report in Annex II}.

The shares in Delphy Groep B.V. (hereinafter: the “Shares”), are held by thirteen (13) shareholders, with individual participation ranging from 1.17% to 16.96%. Delphy Groep B.V. together with its subsidiaries Delphy B.V. and Delphy Projects B.V. form a fiscal entity for the purposes of corporation tax. GreenQ Group B.V. and Improvement Centre B.V. form a (separate) fiscal entity for the purposes of corporate tax.

Management biographies

Jacco van der Wekken

Jacco has a master’s degree in plant cultivation, which master’s degree he achieved in 1988. After finishing his master’s degree, Jacco worked at (among others) The Greenery. After this time Jacco founded Delphy (which was then called DLV Plant Groep). As such, Jacco has been the CEO of Delphy and its (legal) predecessors for over 23 years. Jacco is statutory director of the company.

| 17 |

Arnoud van Boven

Arnoud has achieved a master’s degree at the Erasmus University of Rotterdam. He specializes in agrobusiness and turn-key projects. Arnoud has been with Delphy for over 23 years and is an intrinsic part of its management team.

Aad van den Berg

Prior to working at Delphy, Aad worked as a director at the company Royal Brinkman, which role he fulfilled for 15 years. In 2005 Aad started working as a managing director at Delphy, which role he has (therefore) fulfilled for almost 18 years. Aad specializes in agrobusiness, research projects, and innovation. Since he has joined Delphy, Aad has been a part of the management team.

CORE BUSINESS

Delphys’ core business is the provision of services and advice, with regard to floriculture, pot and bedding plant cultivation, greenhouse vegetable production, ornamental horticulture, fruit cultivation, strawberry cultivation, outdoor vegetable production, cut flowers, agriculture, flower bulbs and other vegetable products. Delphy focusses on business in the primary sector of food production and agricultural resource production.

GreenQ Group B.V. and Improvement Centre B.V. operate a modern greenhouse complex in which new cultivation concepts and technical installations (from all parts of the world) are developed, tested and demonstrated.

According to the Registry of the Dutch Chamber of Commerce, the sole director of Delphy Groep B.V. is Mr. C.J. van der Wekken. As follows from the minutes of meetings from the board, an informal board or management team consists of Aad van den Berg, Jacco van der Wekken, Jeroen van Buren, Gerjo Engbers, Arnoud van Boven, Martine de Jong, Klaas Walraven, and Irma Bellekom.

LOAN AGREEMENTS

The provided Documents contain a number of agreements relating to loans of Delphy, an overview of the loans is as follows the outstanding amounts have been derived from the most recent credit agreement provided, dated August 2021:

| ABN Amro | Credit facility | € | 750,000 | |||

| ABN Amro | Loan | € | 1,100,000 | |||

| ABN Amro | Loan | € | 1,000,000 |

Loan agreement ABN Amro dated 31 January 2014

An agreement between ABN Amro and the companies within the Delphy Group was provided (dated 31 January 2014), relating to a credit arrangement between both parties. The agreement is factually a continuance of an earlier agreement dated 5 September 2011, the general terms and conditions of ABN (as are discussed in this chapter) apply. As security for the credit arrangement, a mortgage has been pledged.

| 18 |

The loan consists of two separate loans (as certain provisions apply to each loan separately), the first being a ‘EURIBOR loan’ for a total of €2,458,333 (of which €1,333,333 was yet outstanding at the time this continued agreement was signed), the second being a ‘loan’ of €1,100,000 (the total amount of which was still outstanding at the time this continued agreement was signed).

Aside from the mortgage, liens were also agreed upon. In accordance with the agreement, liens have been placed on; any and all stock and inventory, receivables owed to the companies, and other goods (as described in the general terms and conditions).

Furthermore, surety was agreed upon, amounting to a surety of €25,000 (plus interest and costs) by P. Klapwijk and a parallel surety by L. van den Berg, also for €25,000,00.

Loan agreement ABN Amro dated 30 May 2020

A later agreement was provided between ABN Amro and GreenQ Group B.V. (dated 30 May 2020), also relating to a credit agreement between both parties. The agreement is a continuance of an earlier agreement dated 6 March 2019, which in turn is a continuance of the loan agreement dated 31 January 2014. As this agreement has been renegotiated, an extensive disquisition on the loan agreement does not seem relevant, therefore, refer to the next part of this paragraph.

Loan agreement ABN Amro doted 13 August 2021

The last loan agreement provided between ABN Amro and GreenQ Group B.V. (dated 13 August 2021) is a continuance of the loan agreement dated 24 June 2020 (which seems to be the signing date of the agreement as set out above). The parties to the agreement are ABN AMRO Bank N.V., and GreenQ Group B.V., Delphy Groep B.V., Delphy B.V., Delphy Projects B.V., and Improvement Centre B.V. As was the case with all previous agreements, the general terms and conditions of ABN (as have been discussed) apply.

The loan now consists of a credit facility of €750,000 and two loans. The first loan amounts to €1,100,000 (of which the entire amount is still outstanding at the time the agreement was signed), and the second loan amounts to €1,000,000 (of which €900,000 was still outstanding at the time the agreement was signed).

The most important arrangements of the agreement are as follows:

| (i) | the interest on the current account is variable, that is to say that it consists of the monthly EURIBOR average plus (+/+) market allowance plus (+/+) an agreed upon increment. When the agreement was signed the following was true of these number: monthly EURIBOR (- 0.557%) + market allowance (0.30%) + increment (2.40%) = 2.143% interest; |

| 19 |

| (ii) | further costs include a credit provision of 0.25% per quarter and a commitment fee of 0.5% per year; | |

| (iii) | The agreement states that the provisions of earlier agreements still apply to both the loans. Furthermore, Delphy Agriconsult B.V., Delphy International B.V. and GreenQ Group B.V. are no longer jointly and severally bound to the loans (as they have ceased to exist). The other parties (as mentioned above) are jointly and severally liable for claims under the agreement; | |

| (iv) | the bank uses certain calculations whereby it is possible that the claim of the bank can become due early; | |

| (v) | it is agreed that the companies must try to use the bank as a vehicle for payments as much as possible; | |

| (vi) | if certain rules and regulations are amended, so shall the agreement be. |

As mentioned above the agreement states that past agreements shall still apply to the loans. However, not all previous agreements have been provided, which means that we have not been able to verify if the sureties of P. Klapwijk and L. van den Berg still apply (no Documents have been provided to that effect, but no Documents entirely disprove the existence of these sureties). While the most recent agreements between Delphy and ABN Amro do not explicitly mention these sureties as part of the arrangements, the agreements do refer to previous agreements, which may mean that suretyship may still apply to the current agreements. Applicability of the sureties would have no adverse effect on the business, however, the sureties apply to two people who would not concur with continued suretyship.

Mortgage agreement ABN Amro

A mortgage agreement has been provided between AMRO Bank N.V., and Delphy Groep B.V. and GreenQ Group B.V. together. The mortgage is placed on the registered properties as mentioned in the agreement, for a maximum amount of €7,000,000 (which consists of a maximum claim against the mortgaged properties of €5,000,000 as principal, and costs up to a maximum of €2,000,000).

The mortgage is placed on the following properties:

Violierenweg 3, 2665 MV Bleiswijk, known to the Municipality of Bleiswijk, section D, number 3112 (the surface of which is 20,080 m2).

Properties on the Dijkgraafweg in Hazerswoude, known to the Municipality of Hazerswoude, section K, numbers 61,657 and 752 (the surface of which amounts to a total of 24,540 m2).

The mortgage has been established for any claim the bank might have on; GreenQ Group B.V., Delphy Groep B.V., Delphy B.V., Delphy Agriconsult B.V., Delphy Projects B.V., Delphy International B.V., Improvement Centre B.V. and GreenQ B.V. (some of which no longer exist). The general terms and conditions of ABN Amro are applicable to the mortgage deed (said terms and conditions are discussed within this chapter). A provisions is made on renting out the properties, whereby the bank must first consent to intended lease of the properties.

| 20 |

As of November 2021, there are 183 employees working at Delphy B.V. and Improvement Centre B.V. Of these employees, 162 are employed by Delphy B.V. and 21 by Improvement Centre B.V. In addition, there are 9 people on the payroll.

The management of Delphy Groep BV is advised by the Advisory Board of Delphy Groep BV. The members of the Advisory Board are appointed by the shareholders of the Delphy Groep BV. The following applies to the Advisory Board: in order to guarantee the independence of Delphy Groep BV, all members sit in a personal capacity.

Long-term debt as of December 31, 2021 and 2020 consists of the following:

| December 31, 2021 | December 31, 2020 | |||||||

| 2.3% Loan payable (€1,000,000 principal) in quarterly installments of €50,000 including interest, with final payment of €50,000 (1 January, 2026)^ . | € | 850,000 | € | 337,988 | ||||

| 1.2% Loan payable (€1,100,000 principal) payable at end of term, including interest, with final payment of €1,100,000 (1 July, 2026)*. | 1,100,000 | 1,100,000 | ||||||

| Total Long-Term Debt | € | 1,950,000 | € | 1,437,988 | ||||

| Less: | ||||||||

| Current installments of long-term debt | 200,000 | 150,000 | ||||||

| Long-Term Debt, Excluding Current Installments | € | 1,750,000 | € | 1.287,988 | ||||

^ Conditions:

Lender: ABN AMRO Bank N.V. Principal amount: €1,000,000

Repayment: €50,000 on the first day of each quarter Interest: 2.3%

Fair value of this long-term debt approximates the carrying value

| 21 |

* Conditions:

Lender: ABN AMRO Bank N.V. Principal amount: €1,100,000

Repayment: full repayment at the end of the term Interest: 3 months Euribor + 1.2%

Fair value of this long-term debt approximates the carrying value

The following securities have been provided:

- A bank mortgage, first in rank, amounting to €5,000,000 on the untaxed registered property located in Hazerwoude, Dijkgraafweg and Bleiswijk, Violierenweg;

- A pledge on stocks;

- A pledge on company inventory;

- A pledge on claims.

REVENUE

The Company generates revenue primarily from the provision of services, conducting research for customers and other services (trainings and subscriptions). In the following table, revenue from contracts with customers is disaggregated by major service lines and timing of revenue recognition. The table also includes revenue from the major business lines.

| December 31, 2021 | December 31, 2020 | |||||||

| Advisory services | € | 11,400,825 | € | 10,810,597 | ||||

| Research | 2,730,588 | 2,587,762 | ||||||

| Other | 2,417,358 | 2,290,916 | ||||||

| Contract balances | € | 16,548,771 | € | 15,689,275 | ||||

The following table provides information about receivables, contract assets and contract liabilities from contracts with customers.

| December 31, 2021 | December 31, 2020 | |||||||

| Trade accounts receivable | € | 3,341,772 | € | 3,166,089 | ||||

| Contract asset | 3,605,535 | 3,933,889 | ||||||

| Contract liability | 4,100,133 | 3,773,132 | ||||||

The contract assets primarily relate to the Company’s rights to consideration for work performed but not billed at the reporting date on research projects. The amount of contract assets during the period ended 31 December 2021 was not impacted by an impairment charge. The contract assets are transferred to receivables when the rights become unconditional. This usually occurs when the Group issues an invoice to the customer.

The contract liabilities primarily relate to fees received by the Company for which the associated performance obligations have not been satisfied and revenue has not been recognized.

The Company has multiple projects which are financed by government grants. In 2020 the Company received Noodmaatregel Overbrugging Werkgelegenheid (NOW) subsidy, which is a temporary emergency COVID-19 support for employment expenses. The table below shows an overview of the subsidy income recognized from various governmental organizations.

| December 31, 2021 | December 31, 2020 | |||||||

| Government grants | € | 7,044,325 | € | 6,607,488 | ||||

| NOW | - | 554,940 | ||||||

| Other | 12,064 | 48,445 | ||||||

| Cost of government grants | (5,642,360 | ) | (4,928,962 | ) | ||||

| € | 1,414,029 | € | 2,281,911 | |||||

| 22 |

Vote Required

The approval of a majority of shares present and voting at this Special Meeting is required to approve Matter 4.

THE BOARD RECOMMENDS A VOTE “FOR”

APPROVAL OF THE DELPHY ACQUISITION AND SHARES TO BE ISSUED IN THE DELPHY ACQUISITION.

MATTER NO. 5 - OTHER MATTERS

The Board knows of no matter to be brought before the Special Meeting other than the matters identified in this proxy statement. However, if any other matter properly comes before the Special Meeting or any adjournment of the meeting, it is the intention of the persons named in the proxy solicited by the Board to vote the shares represented by them in accordance with their best judgment.

| BY ORDER OF THE BOARD OF DIRECTORS | |

| /s/ Ingo Mueller | |

| Ingo Mueller | |

| Chairman and CEO |

| 23 |

ANNEX I

FINANCIAL STATEMENTS FOR DELPHY GROEP BV

| 24 |

Delphy Groep B.V.

Audited Consolidated Financial Statements

As of and for the years ended December 31, 2021 and 2020

| 25 |

| TABLE OF CONTENTS | ||

| INDEPENDENT AUDITORS’ REPORT | 27 | |

| CONSOLIDATED BALANCE SHEETS | 29 | |

| CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME | 30 | |

| CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY | 31 | |

| CONSOLIDATED STATEMENTS OF CASH FLOWS | 32 | |

| NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS | 33 | |

| 1. | BUSINESS OVERVIEW | 33 |

| 2. | BASIS OF PREPARATION | 33 |

| 3. | SIGNIFICANT ACCOUNTING POLICIES | 35 |

| 4. | OTHER CURRENT ASSETS | 40 |

| 5. | PROPERTY, PLANT AND EQUIPMENT | 40 |

| 6. | EQUITY METHOD INVESTMENTS | 41 |

| 7. | OTHER RECEIVABLES | 43 |

| 8. | ACCOUNTS PAYABLE AND OTHER CURRENT LIABILITIES | 43 |

| 9. | LONG TERM DEBT | 43 |

| 10. | OTHER LIABILITIES | 44 |

| 11. | SHARE CAPITAL | 44 |

| 12. | REVENUE | 45 |

| 13. | OTHER INCOME | 45 |

| 14. | INCOME TAXES | 46 |

| 15. | RELATED PARTY TRANSACTIONS | 47 |

| 16. | EMPLOYEE PLAN | 47 |

| 17. | COMMITMENTS AND CONTINGENCIES | 48 |

| 18. | SUBSEQUENT EVENTS | 49 |

| 26 |

To the Board of Directors and Stockholders of Delphy Groep B.V.

Opinion

We have audited the consolidated financial statements of Delphy Groep B.V., which comprise the consolidated balance sheets as of December 31, 2021 and 2020, and the related consolidated statements of income and comprehensive income, changes in stockholder’s equity, and cash flows for the years then ended, and the related notes to the consolidated financial statements.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the consolidated financial position of Delphy Groep B.V. as of December 31, 2021 and 2020, and the consolidated results of its operations and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

Basis for Opinion

We conducted our audits in accordance with auditing standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of Delphy Groep B.V. and to meet our other ethical responsibilities in accordance with the relevant ethical requirements relating to our audits. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Responsibilities of Management for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about Delphy Groep B.V.’s ability to continue as a going concern within one year after the date that the financial statements are available to be issued.

Marcum LLP ■ 600 Anton Boulevard ■ Suite 1600 ■ Costa Mesa, California 92626 ■ Phone 949.236.5600 ■ Fax 949.236.5601 ■ www.marcumllp.com

| 27 |

Auditors’ Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Misstatements are considered material if there is a substantial likelihood that, individually or in the aggregate, they would influence the judgment made by a reasonable user based on the financial statements.

In performing an audit in accordance with GAAS, we:

| ● | Exercise professional judgment and maintain professional skepticism throughout the audit. | |

| ● | Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. | |

| ● | Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of Delphy Groep B.V.’s internal control. Accordingly, no such opinion is expressed. | |

| ● | Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the financial statements. | |

| ● | Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about Delphy Groep B.V.’s ability to continue as a going concern for a reasonable period of time. |

We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal control related matters that we identified during the audit.

Costa Mesa,

CA August 31,

2021

| 28 |

CONSOLIDATED BALANCE SHEETS

(Expressed in EURO)

Note | December 31, 2021 | December 31, 2020 | ||||||||||

| ASSETS | ||||||||||||

| Current | ||||||||||||

| Cash and cash equivalents | € | 4,955,602 | € | 4,721,338 | ||||||||

| Restricted cash | 42,631 | 42,631 | ||||||||||

| Trade accounts receivable, less allowance for doubtful accounts of €32,029 in 2021 and €432,608 in 2020 | 3,341,772 | 3,166,089 | ||||||||||

| Inventories | 17,727 | 19,921 | ||||||||||

| Other current assets | 4 | 4,010,045 | 4,518,962 | |||||||||

| Total current assets | 12,367,777 | 12,468,941 | ||||||||||

| Non-current | ||||||||||||

| Other receivables | 7 | 149,050 | 182,002 | |||||||||

| Equity method investments | 6 | 541,911 | 629,721 | |||||||||

| Property, plant and equipment, net | 5 | 4,639,787 | 3,109,654 | |||||||||

| Intangible assets | 9,911 | 4,570 | ||||||||||

| Total assets | € | 17,708,436 | € | 16,394,888 | ||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||||||

| Current | ||||||||||||

| Accounts payable and other current liabilities | 8 | € | 9,082,180 | € | 8,142,359 | |||||||

| Current installments of long-term debt | 9 | 200,000 | 150,000 | |||||||||

| Income taxes payable | 14 | 78,452 | 330,543 | |||||||||

| Total current liabilities | 9,360,632 | 8,622,902 | ||||||||||

| Non-current | ||||||||||||

| Long-term debt | 9 | 1,750,000 | 1,287,988 | |||||||||

| Other liabilities | 10 | 186,375 | 196,640 | |||||||||

| Total liabilities | 11,297,007 | 10,107,530 | ||||||||||

| Commitments and contingencies | 17 | |||||||||||

| Stockholders’ equity | ||||||||||||

| Common shares, €1 par value per share, 18,000 shares authorized, issued and outstanding at December 31, 2021 and December 31, 2020, respectively | 11 | 18,000 | 18,000 | |||||||||

| Treasury stock | (921,878 | ) | (139,081 | ) | ||||||||

| Additional paid-in capital | 286,108 | 286,108 | ||||||||||

| Retained earnings | 7,005,538 | 6,096,469 | ||||||||||

| Accumulated other comprehensive loss | (3,916 | ) | (4,379 | ) | ||||||||

| Total equity attributable to Delphy Groep B.V. and its subsidiaries | 6,383,852 | 6,257,117 | ||||||||||

| Noncontrolling interest | 27,577 | 30,241 | ||||||||||

| Total stockholders’ equity | 6,411,429 | 6,287,358 | ||||||||||

| Total liabilities and stockholders’ equity | € | 17,708,436 | € | 16,394,888 | ||||||||

The accompanying notes are an integral part of these consolidated financial statements.

| 29 |

CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(Expressed in EURO)

For the years ended December 31, 2021 and 2020

| Note | 2021 | 2020 | ||||||||||

| Revenue | ||||||||||||

| Revenue | 12 | € | 16,548,771 | € | 15,689,275 | |||||||

| Cost of revenue | (7,345,494 | ) | (6,501,617 | ) | ||||||||

| Gross profit | 9,203,277 | 9,187,658 | ||||||||||

| Selling, general and administrative expense | (9,181,496 | ) | (9,893,160 | ) | ||||||||

| Operating income | 21,781 | (705,502 | ) | |||||||||

| Other expense / (income) | ||||||||||||

| Other income, net | 13 | 1,414,029 | 2,281,911 | |||||||||

| Interest income | 29 | 956 | ||||||||||

| Interest expense | (19,109 | ) | (24,345 | ) | ||||||||

| Income of equity method investees | 207,487 | 55,987 | ||||||||||

| Income before income taxes | 1,624,217 | 1,609,007 | ||||||||||

| Income tax expense | 14 | (321,195 | ) | (359,009 | ) | |||||||

| Net income | 1,303,022 | 1,249,998 | ||||||||||

| Net income attributable to non-controlling interest | 4,134 | 6,902 | ||||||||||

| Net income attributable to Delphy Groep B.V. and its subsidiaries | 1,298,888 | 1,243,096 | ||||||||||

| Foreign currency translation adjustments | 463 | 1,465 | ||||||||||

| Net comprehensive income Delphy Groep B.V. and its subsidiaries | € | 1,299,351 | € | 1,244,561 | ||||||||

The accompanying notes are an integral part of these consolidated financial statements.

| 30 |

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(Expressed in EURO, except share numbers)

| Common stock | Treasury stock | |||||||||||||||||||||||||||||||||||||||

| # of Shares | Amount | # of Shares | Amount | Additionl paid-in- capital Retained | Retained earnings | Accumulated other comprehensive income (loss) | Total equity attributable to Delphy Groep B.V. and its subsidiaries | Non~controlling interest | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Balances as of January 1, 2020 | 18,000 | € | 18,000 | 576 | € | (147,192 | ) | € | 282,157 | € | 4,853,373 | € | (5,844 | ) | € | 5,000,494 | € | 23,339 | € | 5,023,833 | ||||||||||||||||||||

Sale of treasury stock | - | - | (37 | ) | 8,111 | 3,951 | - | - | 12,062 | - | 12,062 | |||||||||||||||||||||||||||||

Net income | - | - | - | - | - | 1,243,096 | - | 1,243,096 | 6,902 | 1,249,998 | ||||||||||||||||||||||||||||||

Foreign currency translation | - | - | - | - | - | - | 1,465 | 1,465 | - | 1,465 | ||||||||||||||||||||||||||||||

| Balances as of December 31, 2020 | 18,000 | € | 18,000 | 539 | € | (139,081 | ) | € | 286,108 | € | 6,096,469 | € | (4,379 | ) | € | 6,257,117 | € | 30,241 | € | 6,287,358 | ||||||||||||||||||||

Share repurchase | - | - | 2,069 | (782,797 | ) | - | - | - | (782,797 | ) | - | (782,797 | ) | |||||||||||||||||||||||||||

Net income | - | - | - | - | - | 1,298,888 | - | 1,298,888 | 4,134 | 1,303,022 | ||||||||||||||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | - | 463 | 463 | - | 463 | ||||||||||||||||||||||||||||||

Dividends | - | - | - | - | - | (389,819 | ) | - | (389,819 | ) | (6,798 | ) | (396,617 | ) | ||||||||||||||||||||||||||

| Balances as of December 31, 2021 | 18,000 | € | 18,000 | 2,608 | € | (921,878 | ) | € | 286,108 | € | 7,005,538 | € | (3,916 | ) | € | 6,383,852 | € | 27,577 | € | 6,411,429 | ||||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

| 31 |

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Expressed in EURO)

For the years ended December 31, 2021 and 2020

| 2021 | 2020 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||||||

| Net income | € | 1,303,022 | € | 1,249,998 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Depreciation expense | 305,063 | 228,157 | ||||||

| Provision for jubilee bonuses | (10,265 | ) | (43,076 | ) | ||||

| Net change in allowance for doubtful accounts | (400,579 | ) | 331,005 | |||||

| Equity in income of equity method investees | (207,487 | ) | (63,597 | ) | ||||

| Foreign exchange transaction | (5,874 | ) | 4,256 | |||||

| Changes in operating assets and liabilities: | ||||||||

| Decrease (increase) in trade accounts receivable | 224,896 | (259,759 | ) | |||||

| Decrease (increase) in other current assets | 180,563 | (171,243 | ) | |||||

| Decrease (increase) in other receivables | 26,141 | 20,940 | ||||||

| Increase (decrease) in accounts payable and accrued liabilities | 612,820 | 566,051 | ||||||

| Decrease (increase) in inventories | 2,194 | (2,300 | ) | |||||

| Decrease (increase) in contract assets/liabilities | 655,355 | 2,845 | ||||||

| Increase (decrease) in income tax payable | (252,091 | ) | 363,930 | |||||

| Net cash provided by operating activities | € | 2,433,758 | € | 2,227,207 | ||||

| CASH FLOWS FROM INVESTING ACTIVITIES | ||||||||

| Acquisition of property, plant & equipment | (1,828,662 | ) | (660,468 | ) | ||||

| Acquisition of intangibles assets | (11,875 | ) | - | |||||

| Dividend received | 301,171 | 135,728 | ||||||

| Net cash used in investing activities | € | (1,539,366 | ) | € | (524,740 | ) | ||

| CASH FLOWS FROM FINANCING ACTIVITIES | ||||||||

| Decrease (increase) in receivable from shareholders and associates | 6,811 | (37,648 | ) | |||||

| Proceeds from debt to credit institutions | 662,012 | 337,988 | ||||||

| Principal payments on debt to credit institutions | (150,000 | ) | - | |||||

| Payments to acquire treasury stock | (782,797 | ) | - | |||||

| Proceeds from issuance of common stock | - | 12,062 | ||||||

| Dividend paid | (396,617 | ) | - | |||||

| Net cash (used in) provided by financing activities | € | (660,591 | ) | € | 312,402 | |||

| Effect of exchange rate changes on cash | 463 | 1,460 | ||||||

| Change in cash and cash equivalents | 233,801 | 2,014,869 | ||||||

| Cash and cash equivalents at beginning of year | € | 4,721,338 | € | 2,705,009 | ||||

| Cash and cash equivalents at end of year | € | 4,955,602 | € | 4,721,338 | ||||

| Change in restricted cash | - | 4 | ||||||

| Restricted cash at beginning of year | € | 42,631 | € | 42,627 | ||||

| Restricted cash at end of year | € | 42,631 | € | 42,631 | ||||

The accompanying notes are an integral part of these consolidated financial statements.

| 32 |

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the years ended December 31, 2021 and 2020 (Expressed in EURO, except where noted)

Delphy Groep B.V., Wageningen (the “Company” or “Delphy”) is a Netherland based company and was incorporated as a private company by Articles of Incorporation issued pursuant to the provisions of the Dutch Civil Code on October 11, 2005. The Company’s registered and records office address is at Agro Business Park 5, in Wageningen, the Netherlands and is registered at the chamber of commerce under number 09154407.

The activities of Delphy Groep B.V. and its group companies (“the Company”) mainly focus on the entrepreneurs in the primary sector and agribusiness partners, both nationally and internationally. Advisors in tree cultivation, pot and bedding plant cultivation, greenhouse vegetables, floriculture, fruit cultivation, strawberry cultivation, field vegetable cultivation, cut flowers, arable farming, flower bulbs and other vegetable sectors, are the confidential advisors on the farm of the agricultural entrepreneur.

The two subsidiaries GreenQ Group B.V. and Improvement Centre B.V. operate a modern greenhouse complex, in which new cultivation concepts and technical installations from all parts of the world are developed, tested and demonstrated.

Basis of Presentation

The accompanying consolidated financial statements (the “financial statements”) have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”).

The financial statements and accompanying notes are the representations of the Company’s management, who is responsible for their integrity and objectivity. In the opinion of the Company’s management, the financial statements reflect all adjustments, which are normal and recurring in nature, necessary for fair financial statement presentation.

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of Delphy and its majority-owned subsidiaries (collectively, the Company). All significant intercompany balances and transactions have been eliminated in consolidation.

The Company consolidates entities in which it has a controlling financial interest based on either the variable interest entity (VIE) or voting interest model. The Company is required to first apply the VIE model to determine whether it holds a variable interest in an entity, and if so, whether the entity is a VIE. If the Company determines it does not hold a variable interest in a VIE or the entity is not a VIE, it then applies the voting interest model. Under the voting interest model, the Company consolidates an entity when it holds a majority voting interest in an entity. Immaterial subsidiaries are not included in consolidation.

| 33 |

The Company accounts for investments in which it has significant influence but not a controlling financial interest using the equity method of accounting (see Note 7).

VIE Model

An entity is considered to be a VIE if any of the following conditions exist: (a) the total equity investment at risk is not sufficient to permit the entity to finance its activities without additional subordinated financial support, (b) the holders of the equity investment at risk, as a group, lack either the direct or indirect ability through voting rights or similar rights to make decisions that have a significant effect on the success of the entity or the obligation to absorb the entity’s expected losses or right to receive the entity’s expected residual returns, or (c) the voting rights of some equity investors are disproportionate to their obligation to absorb losses of the entity, their rights to receive returns from an entity, or both and substantially all of the entity’s activities either involve or are conducted on behalf of an investor with disproportionately few voting rights.

The Company consolidates entities that are VIEs when the Company determines it is the primary beneficiary. Generally, the primary beneficiary of a VIE is a reporting entity that has (a) the power to direct the activities that most significantly affect the VIE’s economic performance, and (b) the obligation to absorb losses of, or the right to receive benefits from, the VIE that could potentially be significant to the VIE.

Stichting Participatie DLV Plan Groep (the “foundation”) is a fund established by Delphy to acquire, manage and dispose Delphy’s shares. This foundation is classified as VIE and since Delphy has power to direct most of significant activities of foundation via the director and it has potential significant variable interest, the Foundation is consolidated by Delphy.